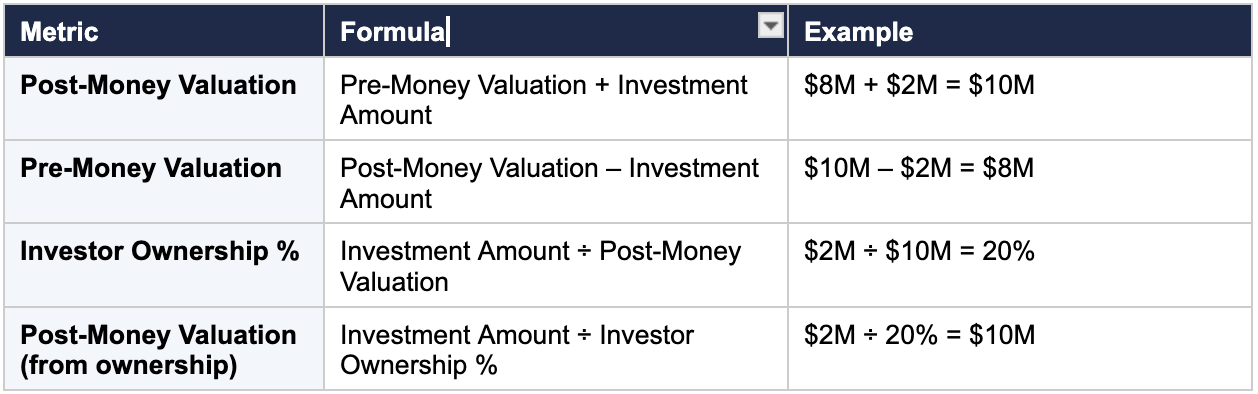

The formula: Post-Money Valuation = Pre-Money Valuation + Investment Amount

Example: $8M pre-money + $2M investment = $10M post-money. The investor owns 20% ($2M ÷ $10M).

Every founder hits the same moment: an investor slides a term sheet across the table, and suddenly the difference between pre-money and post-money valuation determines whether you keep 80% of your company or 65%. Getting this number wrong can cost you millions at exit. This guide breaks down the post-money valuation formula, shows you how to calculate it step by step, and explains why it matters more than most founders realise when negotiating equity with investors.

What Is Post-Money Valuation?

Post-money valuation is the estimated worth of your startup immediately after receiving a new round of investment. It is calculated by adding the investment amount to your pre-money valuation which is the value of the company before the new capital arrives. This single number determines how much of your company each investor owns and sets the baseline for every future funding round.

What is the formula for post-money valuation?

Post-money valuation = Pre-money valuation + Investment amount. For example, if your startup is valued at $8 million before a round and you raise $2 million, your post-money valuation is $10 million. This number determines the investor's ownership percentage for the round.

This concept sounds simple, but the implications ripple through everything: your ownership stake, your co-founders’ equity, your option pool, and your leverage in the next round. A higher post-money valuation means less dilution for existing shareholders. A lower one means you give up more of the company for the same amount of cash.

The Post-Money Valuation Formulas You Need to Know

There are several ways to approach the calculation depending on which variables you have. Here are the core formulas founders and investors use:

The second formula in the table is especially useful during negotiations. If an investor tells you they want 25% of your company for a $3 million investment, you can immediately calculate that they’re implying a $12 million post-money valuation ($3M ÷ 25%), which means a $9 million pre-money valuation. Knowing this lets you negotiate from a position of clarity.

How to get post-money valuation?

There are three ways to calculate it depending on what information you have. If you know the pre-money valuation: add the investment amount to it. If you know the investor's ownership percentage: divide the investment amount by the ownership percentage (e.g. $2M ÷ 20% = $10M post-money). If you know the number of shares: divide the investment amount by the price per share, then add that to the existing share count and multiply by share price.

What is the formula for calculating valuation?

Startup valuation is typically calculated using one of three methods: the revenue multiple method (ARR × industry multiple), the Berkus method (assigning value to key milestones), or the scorecard method (benchmarking against comparable funded startups). At seed stage, most investors use a combination of revenue multiples and qualitative assessment rather than a single formula.

How to Calculate Post-Money Valuation: Step-by-Step

Let’s walk through a realistic example that covers the full calculation, including equity dilution.

Scenario

You’re a SaaS founder with $500K in annual recurring revenue (ARR), growing 15% month-over-month. A venture capital firm offers $4 million for a 20% stake in your company.

Step 1: Calculate the Post-Money Valuation

Post-Money Valuation = Investment ÷ Ownership Percentage ($4,000,000 ÷ 0.20 = $20,000,000)

Step 2: Derive the Pre-Money Valuation

Pre-Money = Post-Money – Investment ($20,000,000 – $4,000,000 = $16,000,000)

Step 3: Understand the Dilution Impact

Before this round, you and your co-founders owned 100% of the company. After the investment, the VC owns 20%, and your collective ownership drops to 80%. If you previously held 60% personally, you now hold 48% of a $20 million company (60% × 80% = 48%). Your stake is worth $9.6 million on paper, compared to $9.6M of a $16M company at 60% ($9.6M). The math works out the same in this example, but future rounds compound the dilution.

Step 4: Factor In the Option Pool

Investors often require that an employee stock option pool (typically 10–20% of the company) be created or expanded before the investment. This pool comes out of the pre-money valuation, meaning it dilutes existing shareholders, not the new investor. If the VC requires a 15% option pool, your effective pre-money valuation drops because that pool is carved from your equity. Always clarify whether the option pool is included in or excluded from the pre-money valuation during negotiations.

Pre-Money vs. Post-Money Valuation: What’s the Difference?

The distinction between pre-money and post-money valuation is the single most misunderstood concept in startup fundraising, and confusing the two during a negotiation can cost founders significant equity.

Pre-money valuation is what your company is worth before the investment. It reflects the agreed-upon value of the business based on traction, revenue, market opportunity, and qualitative factors.

Post-money valuation is what your company is worth after the investment. It always equals the pre-money valuation plus the new capital raised.

Here’s why the distinction matters: if an investor says “I’ll invest $5 million at a $20 million valuation,” you need to know whether they mean $20 million pre-money or $20 million post-money. At $20 million pre-money, the post-money is $25 million and the investor gets 20%. At $20 million post-money, the investor gets 25%. That 5% difference could be worth millions at exit.

5 Startup Valuation Methods That Determine Your Pre-Money Number

Your post-money valuation is straightforward math once you know the pre-money valuation and investment amount. The hard part is arriving at the pre-money number in the first place. Here are the five most common methods investors and founders use:

In practice, most early-stage deals rely on a combination of the Comparable Company method and the Venture Capital method. Investors look at what similar startups raised at, then work backward from their target return to determine what they’re willing to pay for equity today.

Read More: From Pre-Seed to Series E: How Investors Evaluate Startups at Each Round in 2026

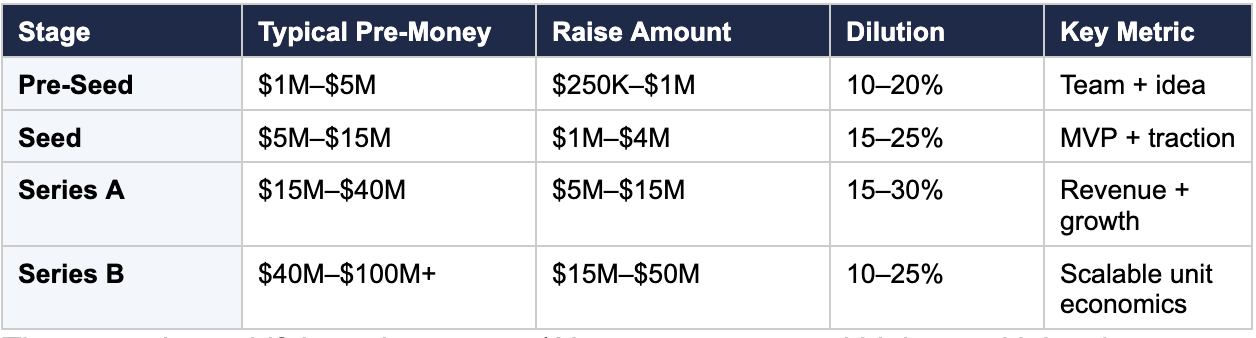

Typical Valuation Ranges by Funding Stage

Valuation norms vary significantly by stage, industry, and market conditions. The ranges below are sourced from Carta’s State of Private Markets Q3 2025 report and the PitchBook-NVCA Venture Monitor, and serve as general benchmarks for US technology startups rather than rigid rules:

These numbers shift based on sector (AI startups command higher multiples than consumer apps in the current market), geography (Silicon Valley valuations tend to run higher than other regions), and macro conditions (rising interest rates generally compress early-stage valuations). Use them as a sanity check, not gospel.

Curious about Fundraising Timelines: How Long It Really Takes to Raise a Round

5 Common Valuation Mistakes Founders Make

These mistakes come up repeatedly in deals that founders later wish they had handled differently, and most of them are straightforward to avoid once you understand the underlying mechanics.

1. Confusing Pre-Money and Post-Money During Negotiations

This happens more often than anyone admits. A founder agrees to a “$10 million valuation” without clarifying whether it’s pre- or post-money. If the raise is $2 million, the difference is between giving up 16.7% of the company (pre-money) and 20% (post-money). Always specify.

2. Ignoring the Option Pool Shuffle

Investors frequently insist that the option pool be sized from the pre-money valuation. This effectively lowers the founders’ effective valuation. A $10M pre-money with a 20% option pool requirement means founders are really working with an $8M effective valuation. Negotiate the pool size carefully and push to include it in the post-money calculation when possible.

3. Anchoring to a Vanity Valuation

A high valuation feels good, but it sets a high bar for the next round. If you raise at $30 million but can’t grow into it, your next round becomes a “down round” — a valuation lower than the previous one. Down rounds damage morale, trigger anti-dilution protections for existing investors, and signal trouble to the market.

4. Not Modelling Future Dilution

Each funding round dilutes existing shareholders. If you plan to raise a Seed, Series A, and Series B, you could go from 100% ownership to under 40% by the time you reach profitability. Model out your cap table across multiple rounds before accepting any term sheet.

5. Relying Solely on Calculator Tools

Online startup valuation calculators are useful for quick math, but they don’t capture the nuances of a real negotiation. Factors like liquidation preferences, anti-dilution clauses, board seat allocations, and pro-rata rights all affect the true economic value of a deal beyond the headline valuation number.

How to Negotiate a Better Post-Money Valuation

Valuation is not purely a math exercise — it’s a negotiation. Here are practical strategies for improving your position:

- Create competitive pressure. Having multiple term sheets (or at least multiple interested investors) is the single most effective way to drive up your valuation. Investors compete on price when they know others are at the table.

- Know your comparables. Research recent funding rounds in your industry and stage. If similar companies raised at 15–20x ARR, you have data to support your ask.

- Focus on the metrics that matter. In 2026, investors prioritise capital efficiency, net revenue retention, and path to profitability over raw growth rate. Highlight the metrics that show sustainable business health.

- Negotiate the option pool separately. Push for the option pool to be included in the post-money valuation, or negotiate a smaller pool size. Every percentage point of the pool that comes from pre-money dilutes founders directly.

- Consider the full term sheet. A slightly lower valuation with founder-friendly terms (no participating preferred, single-trigger acceleration, minimal board seats) can be worth more than a higher valuation with aggressive investor protections.

Frequently Asked Questions

What is the difference between pre-money and post-money valuation?

Pre-money valuation is the agreed-upon value of your startup before new investment capital is added. Post-money valuation is the value after the investment, calculated by adding the investment amount to the pre-money valuation. The distinction directly determines how much equity investors receive: the same investment amount yields a larger ownership stake under a post-money valuation than a pre-money valuation of the same dollar figure.

How do you calculate post-money valuation if you only know the investment and ownership percentage?

Divide the investment amount by the investor’s ownership percentage. For example, if an investor puts in $3 million for 15% of the company, the post-money valuation is $3 million ÷ 0.15 = $20 million. From there, the pre-money valuation is $20 million minus $3 million, or $17 million.

What is a good post-money valuation for a seed-stage startup?

In the current market (2025–2026), seed-stage post-money valuations for US tech startups typically range from $6 million to $20 million, depending on traction, team, and market. SaaS startups with demonstrated product-market fit and early revenue tend to command the higher end of that range. However, valuations vary significantly by geography and sector.

How does equity dilution work across multiple funding rounds?

Each time you raise capital, new shares are issued to investors, reducing the percentage ownership of existing shareholders. If you own 60% after your seed round and raise a Series A where the investor gets 25%, your ownership drops to approximately 45% (60% × 75%). This compounding effect means founders should model dilution across all planned rounds before accepting early-stage terms.

What is the option pool shuffle and why does it matter?

The option pool shuffle is when investors require that an employee stock option pool be created or expanded from the pre-money valuation before their investment. Because the pool comes from the founders’ side of the cap table, it effectively reduces the founders’ valuation. A $10 million pre-money with a 15% option pool means the founders’ effective valuation is only $8.5 million. Understanding this dynamic is essential for negotiating fair terms.

Can I use a startup valuation calculator for fundraising negotiations?

Online calculators are excellent for quick math and understanding the relationships between pre-money valuation, post-money valuation, investment amount, and ownership percentage. However, they cannot account for qualitative factors like term sheet protections, liquidation preferences, board control, or investor reputation. Use calculators as a starting point, but always complement them with legal counsel and experienced advisors.