The median seed round size in 2026 is $3.1M across all industries in the U.S.

By sector:

- AI/ML ~$4.6M

- Healthcare ~$4–5M

- Fintech ~$3.2M

- SaaS ~$2.5–3.2M

- Cybersecurity ~$3–4M

- Climate ~$3–5M

Regional medians:

- Europe €500K–€2.5M

- Africa $1.6M

- Latin America $1–3M.

Seed funding in 2026 looks nothing like it did five years ago. What used to be a handful of small checks from angels has evolved into a structured, institutional asset class where median rounds regularly exceed $3 million and outlier AI deals reach into the billions.

But averages are misleading. The actual seed round size your startup can expect depends heavily on your industry, geography, traction, and whether you have “AI” in your pitch deck. Crunchbase data shows that seed rounds got larger even through the 2022–2024 funding downturn, with larger rounds (above $5M) absorbing a growing share of total seed capital. Meanwhile, smaller rounds became harder to close.

This guide breaks down the median seed round size by industry in 2026, drawing on the latest data from Crunchbase, Carta, CB Insights, PitchBook, and AVCA to give founders everywhere — whether raising in San Francisco, Lagos, London, or São Paulo — a realistic benchmark for how much capital to target and what investors expect in return.

Read more on funding round benchmarks here

The Overall Seed Market in 2026

The global headline: across all industries, the median seed round in the U.S. (which is still the world’s largest venture market) ranges from $2.5 million to $3.5 million, with a median of approximately $3.1 million, based on aggregated deal data. But this number obscures enormous regional variation. In Europe, typical seed checks from new funds range from €500K to €2.5M. In Africa, the median seed round rose 26% in 2025 to $1.6 million, while seed rounds in Latin America generally fall between $1–3M. The Middle East has quietly overtaken Europe as the second-most valuable region for pre-seed deals, with average valuations of $3.7M.

The mathematical average is misleading everywhere, particularly in the U.S., where it sits at roughly $5.6 million because a few massive outlier rounds (including two separate $2 billion AI seed rounds) pull the mean far above what most founders actually raise.

Several structural forces are shaping the global seed market:

- The AI premium: AI startups command median deal sizes of approximately $4.6M, over $1M more than the broader market, according to CB Insights’ Q2 2025 report.

- The barbell effect: Top-tier companies with strong traction raise $3–5M at premium valuations, while many others struggle to close any round at all. The middle is thinning.

- Seed is the new Series A: Based on what we see at Pitchwise, the seed environment in 2026 mirrors what Series A looked like just a few years ago, with investors demanding $300K–$500K in ARR and clear unit economics.

- Fewer but larger rounds: Deal volume has dropped from peak 2021 levels, but the rounds that do close are bigger. Carta’s State of Seed report confirms 2025 was on track to be the biggest year for seed cash raised since 2022.

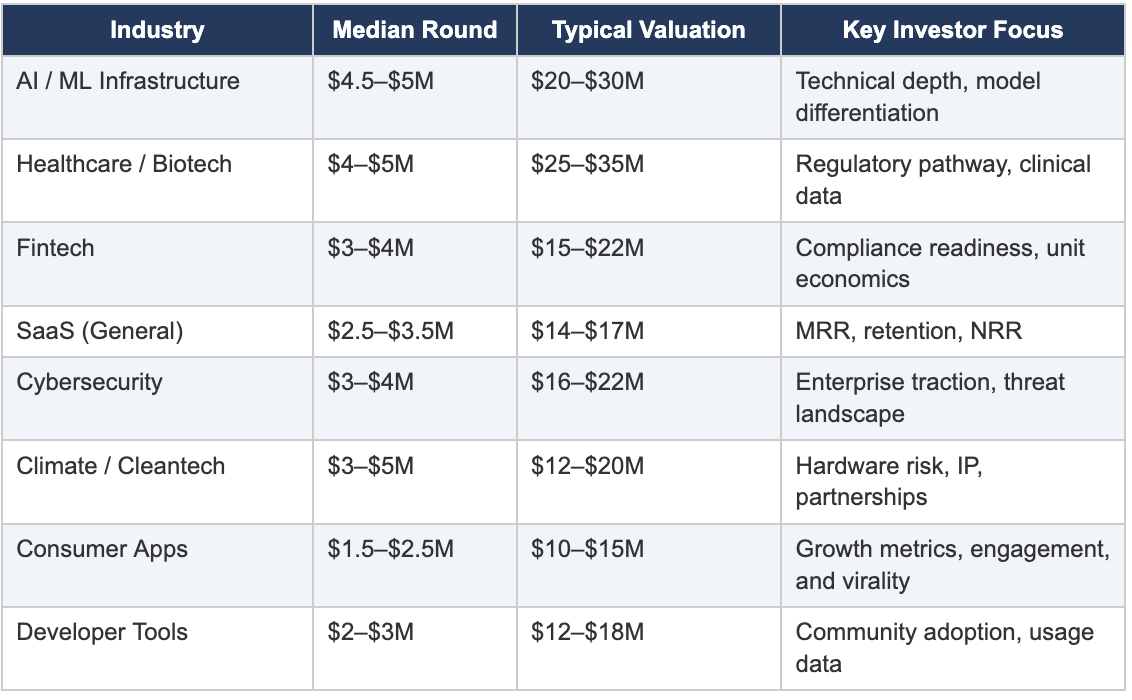

Median Seed Round Size by Industry

The following table synthesises benchmark data from Crunchbase, Carta, CB Insights, and industry reports. These figures are anchored in U.S. market data but broadly reflect global patterns, and with the understanding that founders raising in Europe, Africa, Latin America, and Southeast Asia should apply a regional discount (see the regional section below). All data reflects 2025–2026 conditions.

Median Seed Round Size by Industry

Let’s break each industry down in more detail.

AI and Machine Learning

AI is the undisputed leader in seed round sizes. According to CB Insights’ Q2 2025 data, AI startups command a median deal size of $4.6M — carrying a 1.3x premium over the broader seed market. Valuations for AI companies run 1.6x higher than non-AI comparables, and average round sizes are 1.4x larger.

The extremes are staggering. Bloomberg reported that Mira Murati’s Thinking Machines Lab debuted with a $2 billion seed round at a $12 billion valuation — a figure so extreme it is reshaping how the industry defines “seed.” These outliers skew averages but do not represent what typical AI founders should expect.

For most AI seed-stage companies, the realistic range is $3–5M. Investors are looking for teams with genuine technical depth — not just “AI” in the pitch deck. Over 50% of Y Combinator’s Spring 2025 batch was building agentic AI solutions, which means competition for seed capital in this space is fierce.

Healthcare and Biotech

Healthcare and biotech seed rounds consistently rank among the largest, with a median of approximately $4–5M. This premium reflects longer development cycles, significant regulatory requirements, and the capital-intensive nature of clinical development.

Reports have highlighted healthtech as the third-largest industry by total cash invested at the pre-seed stage, with some of the highest valuation caps in the market and a median of $35 million for rounds of at least $2.5M. This premium pricing carries through to seed.

Investors in this space care deeply about regulatory pathway clarity, the strength of clinical data or preclinical results, and the credibility of the scientific team. Biotech founders should expect longer fundraising timelines and should budget accordingly.

Fintech

Fintech seed rounds land in the $3–4M range, with a median of approximately $3.2M according to current market data. Valuations typically range from $15–$22M pre-money, reflecting both the sector’s strong fundamentals and regulatory complexity.

Fintech faces a unique challenge: regulatory headwinds create both barriers to entry and reasons for investors to demand more proof of compliance readiness before writing checks. Founders raising in this space should have a clear compliance strategy and demonstrate strong unit economics (particularly around CAC payback and net revenue retention) to justify premium seed pricing.

See our guide to fundraising metrics → Startup KPIs That Actually Matter for Investors in 2026

SaaS (General)

General SaaS remains the broadest and most competitive seed category. Metal’s 2025 benchmark report places the median U.S. SaaS seed round between $2.5–$3.2M, with valuations ranging from $14–$17M and typical dilution of 12–15%.

The key distinction in SaaS is between AI-enabled and traditional SaaS. Carta’s data now splits SaaS companies into AI and non-AI categories due to meaningfully different median valuations. AI-enhanced SaaS products command a significant premium, while traditional SaaS requires stronger revenue metrics to close a seed round.

Growth rate matters more than absolute revenue at seed. Companies demonstrating 100–200% year-over-year growth with strong retention can raise successfully even with modest topline numbers.

Cybersecurity

Cybersecurity seed rounds fall in the $3–4M range, benefiting from persistent enterprise demand and an increasingly complex threat landscape. Cybersecurity is among the high-growth sectors driving renewed investor confidence in early-stage funding.

Investors in this space prioritize enterprise traction and large contract potential. Cybersecurity startups that can demonstrate real deployments with recognised customers or compliance-driven demand often command premium valuations at seed.

Climate and Cleantech

Climate and cleantech seed rounds span a wide range — from $3M for software-centric plays to $5M or more for hardware-intensive ventures. The variance reflects the sector’s diversity: a carbon accounting SaaS platform has very different capital requirements than a hydrogen fuel cell startup.

European investors have been particularly active in this space, with multiple new climate-focused funds launching in H2 2025. Investors typically look for strong IP, strategic partnerships with established players, and a clear path through what can be lengthy hardware development and certification cycles.

Consumer Apps

Consumer apps represent the most challenging seed fundraising environment. Median rounds sit between $1.5–$2.5M — the lowest of any major category — reflecting investor caution and the difficulty of predicting consumer behaviour at scale.

Founders in this space need exceptional engagement metrics, strong user growth trajectories, and clear evidence of virality or network effects. Without these, consumer rounds are difficult to close at meaningful sizes.

How Seed Round Sizes Have Changed: 2021–2026

To understand where we are, it helps to see the trajectory. The following table tracks how median seed round sizes, valuations, and dilution have evolved across the boom, downturn, and recovery:

The key takeaway: seed rounds have structurally gotten larger. Even the 2023 downturn only temporarily compressed sizes before the AI-driven recovery pushed medians to new highs. Crunchbase confirms that since 2022, seed rounds above $5M have received more total investment than rounds of $5M or less. This is a dramatic shift from how seed capital was distributed historically.

How Seed Rounds Differ by Region

Seed round benchmarks are not universal. Geography is one of the strongest determinants of round size, valuation, and dilution. Here is how the major regions compare:

United States: The deepest and most mature seed market, with a median round of $2.5–$3.5M and pre-money valuations around $14–$20M. AI startups command significant premiums. Dilution typically sits at 15–20%. The U.S. remains the global benchmark, but competition for investor attention is intense.

Europe: European seed rounds typically range from €1–2.5M, with new funds often writing initial checks between €500K and €2.5M. Valuations tend to be more conservative than the U.S. — roughly 20–30% lower for comparable companies. Dilution averages around 21%. However, Europe’s seed ecosystem is maturing rapidly, with London, Paris, and Berlin as established hubs and strong new fund activity across the Nordics, Baltics, and Central and Eastern Europe.

Africa: Africa’s seed market is the continent’s strongest funding stage. According to the 2025 AVCA report, seed and early-stage deal activity expanded with median deal sizes reaching multi-year highs. The median African seed round reached $1.6M in 2025, which is a 26% increase year-on-year. Fintech dominates (46% of deals), but cleantech has emerged as a serious contender. Investors increasingly expect hard-currency revenues and strong unit economics. Dilution tends to be higher (20–30%) due to perceived risk premiums.

Middle East: The Middle East has quietly become a significant seed market, overtaking Europe as the second-most valuable region for pre-seed deals with an average pre-seed valuation of $3.7M. The UAE, Saudi Arabia, and Qatar are driving this growth through sovereign-backed programs, tech-friendly regulatory environments, and an expanding base of local VCs. Dilution is higher on average (around 24.8%), but capital availability is growing rapidly.

Latin America: The Latin American seed market reached over $1 billion in pre-seed and seed rounds in 2022 and has since stabilised. Typical seed rounds range from $1–3M, with fintech and e-commerce leading sector activity. Founders often dilute 20–30% (higher than U.S. peers) due to risk premiums. Brazil and Mexico anchor the region’s deal flow.

Southeast Asia: Southeast Asian seed rounds generally fall between $1–3M, with Singapore serving as the regional hub. The market benefits from strong government co-investment programs and growing interest from global investors. Fintech, logistics, and agritech drive deal flow across Indonesia, Vietnam, the Philippines, and Thailand.

See our region-specific investor lists → Top 50+ VCs in Each Market: Europe, US, UK, Africa & LatAm (2026 Edition)

What This Means for Founders Raising in 2026

Understanding benchmarks is useful, but turning them into a fundraising strategy is what matters. Here is how to apply this data:

Size your round to milestones, not benchmarks. The right amount to raise is the amount that gets you to your next fundable milestone — typically 18 months of runway. Work backwards: define your Series A milestones, calculate the burn rate needed to get there, add a 30% buffer, and that is your target raise.

Calibrate expectations to your industry. If you are building a consumer app, do not anchor on the $4.6M AI median. Your investors have different return profiles, risk tolerances, and benchmark expectations. Use industry-specific data, not market-wide averages.

The bar for traction is higher than ever. Per our research, many seed investors in 2026 expect $300K–$500K in ARR, early evidence of efficient growth, and clear unit economics. The days of raising seed on a pitch deck and a prototype are largely over — except for repeat founders and exceptional technical teams in AI.

Dilution discipline matters. Across all sectors, founders are typically giving up 15–20% equity at seed. Data shows a consistent median of 20% across the last seven quarters. Raising too much at a low valuation compresses your equity ahead of Series A, so balance round size against dilution carefully.

Present yourself professionally. In a competitive market where investors see hundreds of deals, how you present your materials matters. Tools like Pitchwise allow founders to share their deck via a trackable link, monitor investor engagement slide-by-slide, and manage their data room — all for a fraction of the cost of enterprise alternatives like DocSend.

What the benchmarks mean for your raise

Knowing the median matters, but it's only useful if you know where you sit relative to it. If you're raising below the median for your sector, that's not automatically a problem, it means you need stronger traction signals to compensate, or a clear narrative for why your round is sized the way it is.

A few practical takeaways:

- If you're in AI, don't let the $4.6M median pressure you into raising more than you need. Outlier rounds are skewing that number significantly.

- If you're in Africa, Latin America, or Southeast Asia, apply a 40–60% regional discount to U.S. benchmarks. Raising to local norms with a credible plan is more fundable than chasing U.S. round sizes.

- If you're in SaaS, growth rate matters more than absolute revenue at seed. 100–200% YoY growth with strong retention can compensate for modest topline numbers.

- When you're ready to share your deck with investors, Pitchwise gives you slide-level analytics so you can see exactly which investors are engaged and follow up at the right moment.

Frequently Asked Questions

What is the average seed round size in 2026?

The median U.S. seed round in 2026 is approximately $3.1 million across all industries. However, the mathematical average is higher (around $5.6M) due to outlier AI rounds in the billions. Medians are a more reliable benchmark for most founders. Industry matters significantly: AI and healthcare rounds run $4–5M, while consumer apps average $1.5–2.5M.

How much equity do founders give up in a seed round?

Founders typically dilute 15–20% at the seed stage. AI startups at the end may dilute as little as 10.5% in hot rounds, but this is rare. Dilution depends on round size, valuation, and negotiating leverage.

How has AI affected seed round sizes?

AI has had an outsized impact. AI startups command a median deal size of roughly $4.6M, a 1.3x premium over the broader market. Valuations for AI companies run 1.6x higher than non-AI comparables. However, this premium is reserved for teams with genuine technical depth, not companies that simply add “AI” to their pitch deck. The rise of agentic AI has created intense competition at seed, with over half of YC’s Spring 2025 batch building in this space.

Is it harder to raise a seed round in 2026?

It depends on where you sit. Overall seed deal volume has declined from peak 2021 levels, meaning fewer companies are getting funded. But the companies that do close rounds are raising more capital at higher valuations. The market rewards founders with strong traction, efficient growth, and clear paths to profitability. For well-prepared founders, the environment is favourable. For those without meaningful traction, the bar is meaningfully higher than it was three years ago.

Should I use a SAFE or priced round for my seed raise?

In 2025–2026, the majority of seed rounds under $4M are structured as SAFEs (Simple Agreements for Future Equity). SAFEs are faster and cheaper to execute. For rounds above $3M or those with complex cap tables, priced equity rounds offer more clarity for both founders and investors. The right choice depends on your round size, investor preferences, and how clean your existing cap table is.