By clicking “Accept All Cookies”, you agree to the storing of cookies on your device to enhance site navigation, analyze site usage, and assist in our marketing efforts. View our Privacy Policy for more information.

A SAFE is simple to sign and easy to misunderstand. You take the money, the investor gets a document, and nothing happens to your cap table yet. Then your priced round arrives and suddenly shares are being issued, ownership percentages are changing, and you are trying to work out whether the number of shares makes sense.

This article explains exactly how a SAFE converts, what determines the number of shares issued, and what your dilution looks like under different terms. There is a free calculator at the end where you can run your own numbers.

What a SAFE is

SAFE stands for Simple Agreement for Future Equity. It is an investment instrument originally designed by Y Combinator that lets an investor put money into a startup today in exchange for the right to receive shares later, when the company raises a priced equity round.

A SAFE is not a loan. There is no interest rate and no maturity date on a standard SAFE. The investor does not get repaid in cash. They receive shares when the conversion event happens, at a price determined by the terms of the SAFE.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

Two terms control the conversion: the valuation cap and the discount rate. They can be used separately or together. The combination of both is the most common structure for early-stage SAFEs.

Valuation cap

The valuation cap sets the maximum valuation at which the SAFE investor's money converts. If you raise a priced round at a valuation higher than the cap, the SAFE investor converts as if the valuation were only as high as the cap. This rewards early investors by ensuring they get more shares than later investors when the company has grown.

Example: an investor holds a SAFE with a $3,000,000 valuation cap. You raise a Series A at a $3,800,000 pre-money valuation. The SAFE investor converts at $3,000,000, not $3,800,000. Their price per share is lower, so they receive more shares for the same investment amount.

Discount rate

The discount rate gives the SAFE investor a percentage reduction on the price per share paid by new investors at the priced round. A 20% discount means the SAFE investor pays 80% of whatever the new investors pay per share.

Example: new investors at your Series A pay $3.80 per share. A SAFE investor with a 20% discount pays $3.04 per share. For the same investment amount, they receive more shares than the new investors.

When both terms apply: the MFO rule

When a SAFE has both a valuation cap and a discount rate, the investor gets whichever term gives them more shares. This is called the Most Favourable Option, or MFO. You do not add the two benefits together. The investor picks the better of the two calculations.

A worked example

Here are the inputs for a single SAFE conversion:

Investment amount: $25,000. Valuation cap: $3,000,000. Discount rate: 20%. Shares currently issued: 1,000,000. Predicted valuation at equity round: $3,800,000.

Step 1: Calculate the price per share at the priced round.

Round price per share = $3,800,000 / 1,000,000 shares = $3.80 per share.

Step 2: Calculate the cap price per share.

Cap price per share = $3,000,000 / 1,000,000 shares = $3.00 per share.

Step 3: Calculate the discount price per share.

Discount price per share = $3.80 x (1 - 0.20) = $3.04 per share.

Step 4: Apply MFO. The cap gives a price of $3.00. The discount gives $3.04. The lower price gives the investor more shares, so the cap applies.

Step 5: Calculate shares issued.

Shares = $25,000 / $3.00 = 8,333 shares.

Step 6: Calculate ownership.

Ownership = 8,333 / (1,000,000 + 8,333) = 0.83%.

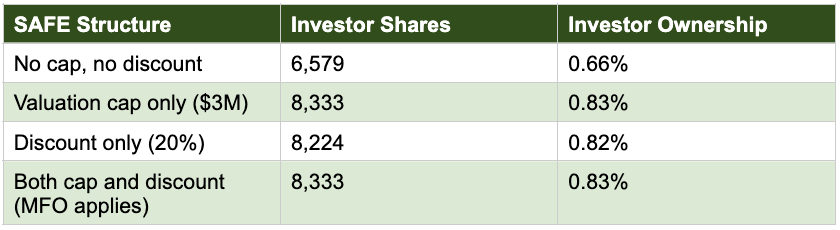

How the four SAFE structures compare

Using the same inputs, here is what each version of the SAFE produces at conversion:

The four SAFE structures compare

The no-cap, no-discount structure gives the investor the fewest shares and the smallest ownership percentage. Every additional term the investor negotiates, whether a cap, a discount, or both, increases the number of shares they receive at conversion.

What happens when you have multiple SAFEs

Multiple SAFEs convert at the same-priced round, each with their own terms. The dilution adds up. Here is what three angels converting at the same $3,800,000 round looks like:

How multiple SAFEs can convert at the same-priced round, each with their own terms.

Three angel SAFEs totalling $115,000 result in 3.43% dilution at conversion. The founders retain 96.57%. Each SAFE is calculated independently before the totals are summed.

The order of SAFE terms matters here. Angel 2 invested twice as much as Angel 1 but has a higher cap and a lower discount. At a $3,800,000 round, both caps are below the round valuation, so both investors convert at their cap price. Angel 2's higher cap means a higher conversion price per share, so they receive fewer shares per dollar invested than Angel 1.

Frequently Asked Questions

What happens if the company never raises a priced round?

Standard SAFEs do not have a maturity date, so there is no automatic repayment if a priced round never happens. What occurs in that situation depends on the specific terms of the SAFE and any side agreements with the investor. Some SAFEs include a dissolution clause that prioritises investor payouts if the company winds down. Consult the specific SAFE document and a lawyer for anything beyond the standard case.

Does the SAFE convert on the pre-money or post-money valuation?

The original YC SAFE used a pre-money valuation cap. YC updated the standard SAFE in 2018 to use a post-money valuation cap. The difference affects how dilution is calculated, particularly when multiple SAFEs convert at the same round. If you are working with older SAFEs or non-standard documents, check which method applies. The Pitchwise simulator uses the pre-money mechanics.

What is the difference between a SAFE and a convertible note?

A convertible note is a loan that converts to equity. It carries an interest rate, typically 5-8%, and a maturity date, usually 12-24 months. If the company has not raised a priced round by the maturity date, the note becomes repayable, or the terms need to be renegotiated. A SAFE is not a loan, has no interest, and has no maturity date in its standard form. SAFEs are simpler and have fewer moving parts for early-stage rounds.

Can I negotiate the cap and discount independently?

Yes. A SAFE can have only a cap, only a discount, both, or neither. Each term is negotiated separately. A cap-only SAFE with no discount is common for early angels who want upside protection without adding complexity. A discount-only SAFE is less common but exists. A SAFE with both terms gives the investor the most protection and is worth modelling carefully before you agree to it.

What does "fully diluted" mean for the share calculation?

'Fully diluted' means the total share count, including your option pool. If you have issued 1,000,000 shares to founders and reserved 100,000 for an employee option pool, the fully diluted count is 1,100,000. Always use the fully diluted count when calculating price per share and ownership percentages. Using only issued shares understates the dilution from the option pool.

Model your own SAFE conversion

The Pitchwise SAFE Ownership Simulator is a free Google Sheets calculator that handles single and multi-SAFE conversions. Enter your investment amount, cap, discount rate, current share count, and predicted round valuation. The model calculates conversion price, shares issued, and ownership percentage for each structure. Download it here.

If you are preparing for a raise and need to share your pitch deck and due diligence documents with investors, Pitchwise gives you document tracking and a data room at $24 a month.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.